High debt levels can be seen in working life–more money talk needed

Minna Markkanen tells that many try to prop up their finances too long by taking out another loan to pay off the old one. Photo: Nelli Kivinen

Minna Markkanen tells that many try to prop up their finances too long by taking out another loan to pay off the old one. Photo: Nelli Kivinen

Over-indebtedness is so widespread among households that it shows in working life too. Minna Markkanen of the Guarantee Foundation says that the people who come to them for help are typically middle-aged women working in the care or retail sectors.

Development Manager Minna Markkanen is sitting in a meeting room in Helsinki’s Pasila district. We are at the Guarantee Foundation, where for years her job has been to monitor people’s debt problems. Statistics show that the Finns are now more heavily in debt than ever. Default levels have been going up all through the 2000s – now the numbers are staggering:

“In September almost 10 per cent of the adult population were listed as bad debtors. This is more than in the recession of the 1990s. A full 15 per cent of men aged 25-44 are listed as bad debtors”, Markkanen says.

“Over-indebtedness is so common that it can also be seen in working life”, Markkanen says.

The Guarantee Foundation uses Veikkaus funding to help people with debt problems by guaranteeing them a loan so that they can combine their old loans into one loan on reasonable terms.

“Our typical customer is a middle-aged woman who lives alone or is a single parent. She is likely to be in a low-paid job in the care or retail sector”, Markkanen says.

“The person will have a low, irregular income with no financial buffers, and their housing is expensive”, says Markkanen, listing the problems typical of the route into over-indebtedness:

The worker’s finances will be poorly managed – their income will vary wildly and credit is far too readily available. Money matters can be derailed by a relationship breaking down. Or the person becomes unemployed or falls ill.

Markkanen says that people with money difficulties are afraid of going on a bad debt register, because it can mean their debt problems suddenly spiral out of control.

“The worker panics and takes out another loan to pay off the old one. They try to prop up their finances in this way for too long.”

“Many of our customers say, if only they had known that wasn’t the right thing to do!”

Rather than getting into a spiral of debt, at that point people should dare to stop and look for help, for example from the financial and debt counselling services of the legal aid offices or the Guarantee Foundation.

If over-indebtedness shows at the workplace in the form of problems with coping, for example, then workplaces can also help people to put their lives in order. Markkanen says it ought to be easier to talk about money matters at work and dare to talk about debt problems too. She would like to break down the taboo surrounding money difficulties.

There is already a model in place for employers to help people with debt problems. The Tradeka group has started a project with the Guarantee Foundation whereby the employer guarantees a loan facility for employees who seek help.

Markkanen hopes the model will spread to other companies too. It’s certainly not in the interest of employers if money matters are keeping employees awake at night and they can’t concentrate on their job properly.

“Studies have shown there is a link between money and debt problems and mental health problems and reduced cognitive capacity.”

Every year around half a million people in Finland have debts recovered. In September around 385,700 people were registered as bad debtors.

“You don’t go on the bad debt register straight away, if a fine, tax or other public debt are collected via debt recovery procedures. You can avoid going on the register if you manage to pay these recovered debts in a reasonable period. But if you have unpaid bank debt, you will go on the register before debt recovery if the district court has ordered the debt to be paid”, Markkanen summarises.

According to Suomen Asiakastieto, you can find yourself in default if a payment remains due for long enough, and in consumer credit this is over 60 days.

You can also get a default entry from a debt recovery service.

Debt default entries make it hard to move home, for example, or to make an agreement where your credit record matters. It can also be the thing that finally puts an end to uncontrolled borrowing.

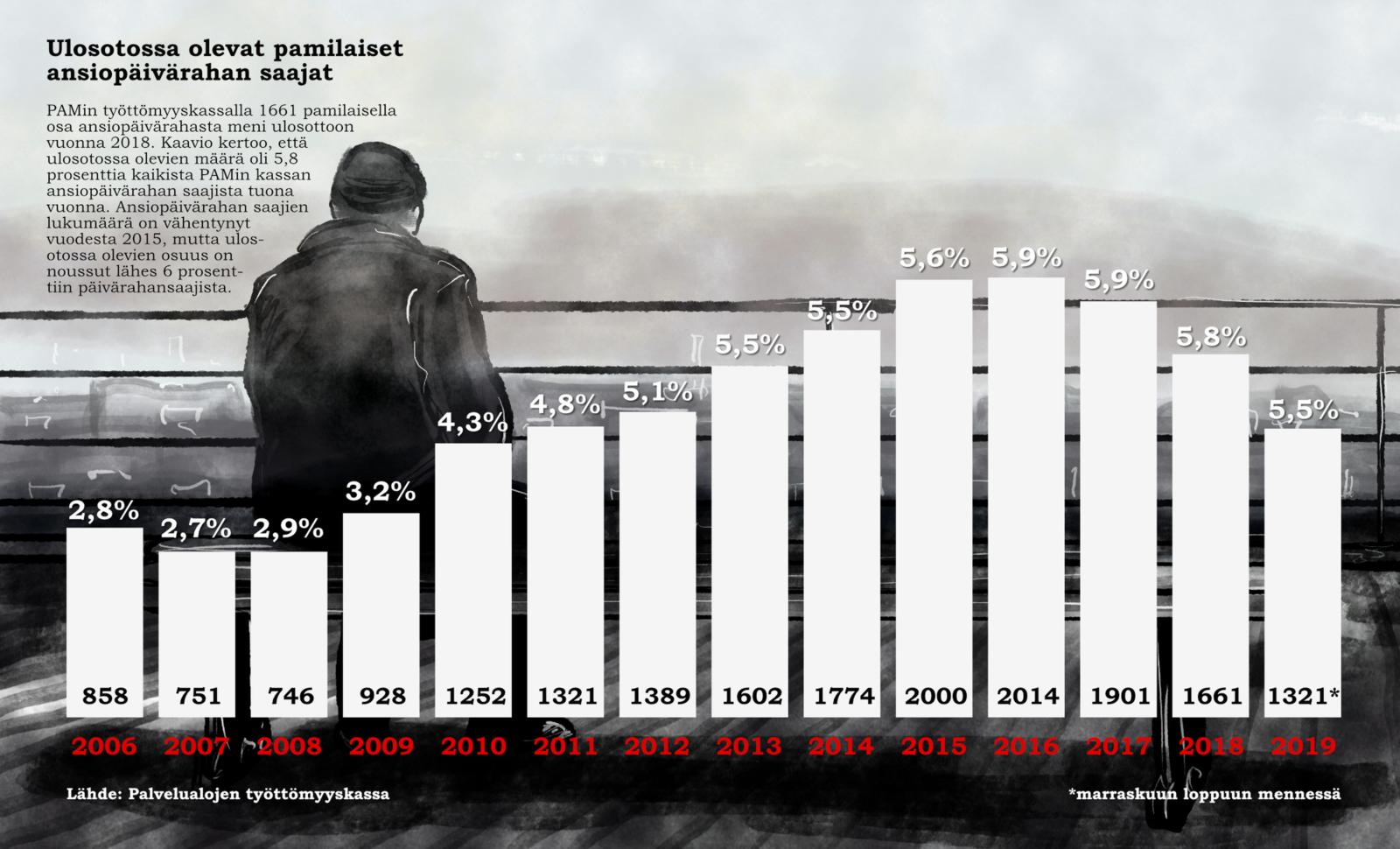

Even though the retail sector is overrepresented in the Guarantee Foundation’s customers, there are no statistics on how many PAM members have part of their pay taken by debt recovery.

However, PAM’s unemployment fund is familiar with payment bans coming from debt recovery bodies. Last year the fund had to withhold part of the allowances of almost 6 per cent of recipients of earnings-related unemployment benefits for debt recovery.

Markkanen points out that anybody can end up with debt problems in today’s world of aggressive lending– there’s no point in blaming yourself and feeling shame.

“My other piece of advice is: don’t keep it to yourself. If in any way you think you can’t manage your credit card payments and loans, seek out help."

Seek help:

Legal Aid Offices, financial and debt counselling

Read more about debt default entries (In Finnish).